A Category in Recalibration: Home Care’s Next Phase

by Nidhi Agrawal

Feb 13, 2026 | 06 min read

Share:

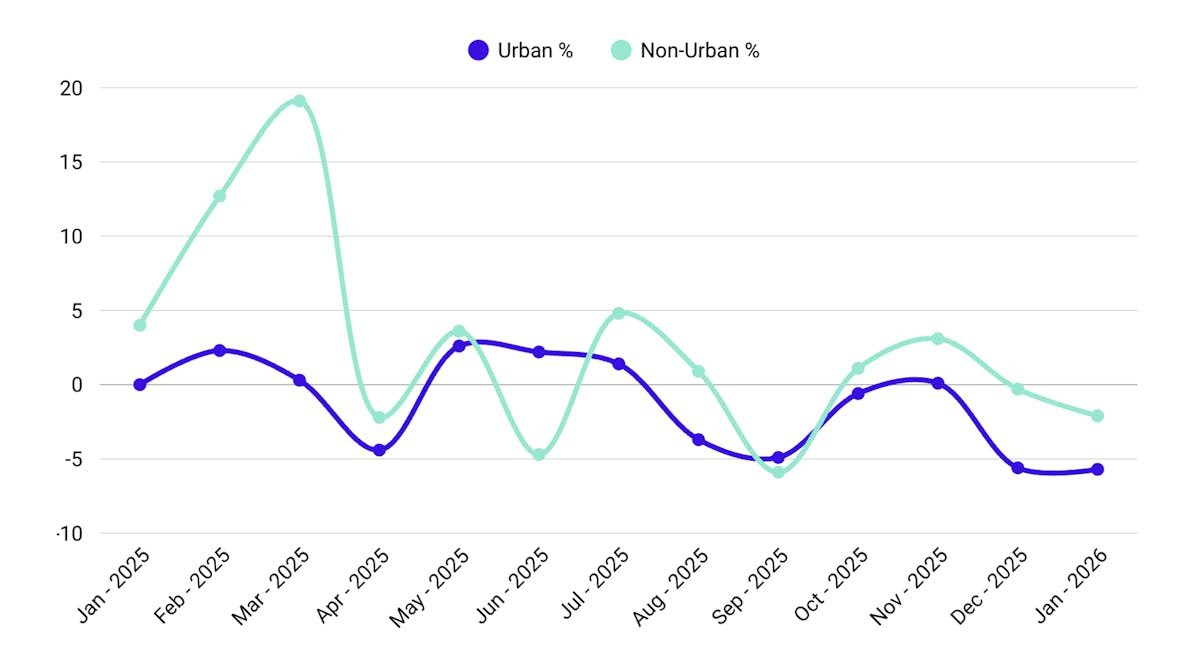

After a year of sharp swings and brief recoveries, the home care category has entered 2026 on a cautious note. Overall, the sector declined by 3.3% YoY in January. The headline may look worrying, but the deeper story is more nuanced.

Urban markets fell by 5.7% YoY, dragging down the average. Non urban markets declined by 2.1% YoY, showing relatively better stability. The gap between the two continues to define the category.

Rewinding to 2025: A Year of Swings

February and March delivered strong YoY growth of 9.1% and 12.8% respectively. Rural markets led that momentum, expanding by 12.7% in February and 19.1% in March.

Urban growth during this period remained modest. The energy clearly came from non urban India.

April brought the first correction, with overall growth turning negative. What followed was a stop start pattern. May and July showed mild recovery. June, August and September pulled the category back. September was the sharpest dip at – 5.6% YoY, with both urban and rural markets under pressure.

The festive quarter did not fully reverse the trend. October and November improved slightly, but December closed at – 2.1% YoY. Urban demand weakened sharply in December, while rural markets were almost flat.

By January 2026, the softness extended across both segments.

The Urban Rural Divide

For much of 2025, non urban India acted as the growth engine. Even in weaker months, rural markets were less volatile. Urban markets showed sharper highs and deeper lows.

Now, both segments are cautious. But urban softness is more pronounced. This suggests pressure on discretionary spends in cities, along with tighter inventory management by retailers.

For brands, this divergence is critical. A uniform strategy will not work. Market specific execution will matter more than ever.

What Kirana Orders Reveal

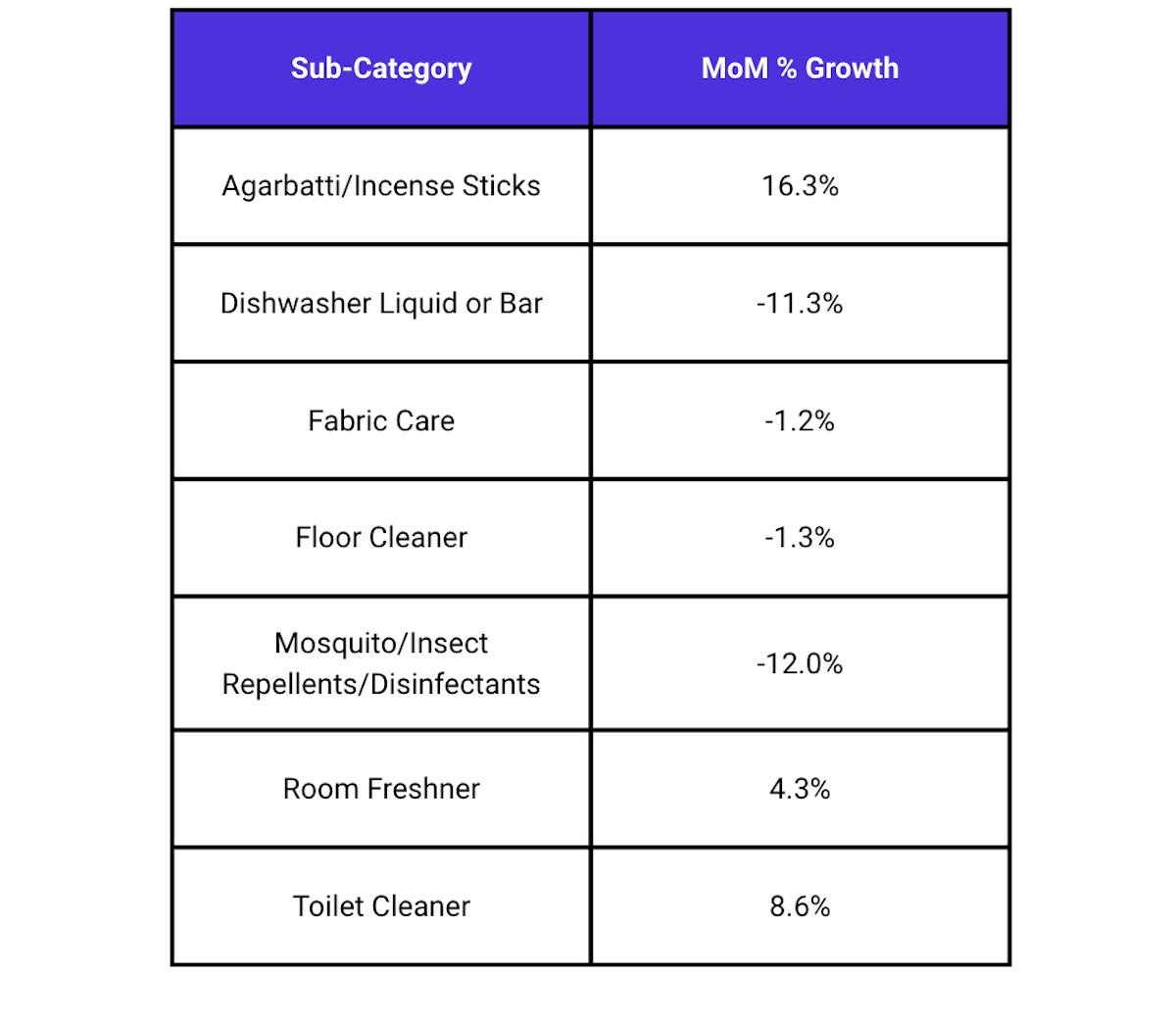

The sub category view adds sharper insight into retailer behaviour.

Agarbatti and incense sticks grew by 16.3% YoY in January 2026. Toilet cleaners expanded by 8.6% and room fresheners grew by 4.3%.

On the other hand, dishwasher liquids and bars declined by 11.3%. Mosquito and insect repellents fell by 12%. Fabric care and floor cleaners were slightly negative.

This pattern tells a clear story. Retailers are prioritising categories with assured rotation and consistent consumer pull. Hygiene linked essentials like toilet cleaners are holding strong. Products linked to rituals and freshness are also seeing traction.

Meanwhile, some core cleaning staples are facing slower movement, leading kiranas to reduce orders.

Signals for Brands

Retailers appear to be managing working capital tightly. They are focusing on fast moving stock and trimming slower segments. In urban markets, sharper volatility means brands must support sales with better visibility, smarter promotions and relevant pack sizes.

In non urban markets, resilience remains, but growth is no longer automatic. Distribution strength and outlet engagement will be key to prevent further slowdown.

Portfolio strategy will also need review. Categories linked to everyday hygiene and household rituals are showing relative strength. These may offer short term growth cushions.

A Category in Recalibration

Home care is not in decline structurally. It is adjusting to a more measured consumption environment.

After a volatile year, both brands and retailers are recalibrating. The opportunity lies in reading these signals early. Which categories are truly resilient. Which markets are stabilising. Which price points are sustaining offtake.

As 2026 progresses, growth will favour those who act with clarity and speed. Home care remains an everyday necessity. But disciplined execution, sharper assortment and market specific playbooks will define who wins the next phase.

The shelves are speaking. The question is, are you listening?

PS: We are releasing the January edition of our Kirana Pulse Report next week. If you would like a copy, reply to this email and we will share it with you.