Kirana Pulse October 2025: India Reveals Its Hidden Appetite

by Aftab Sheikh

Nov 20, 2025 | 04 min read

Share:

October delivered growth, but more importantly, it delivered clues.

Subtle shifts in kirana behaviour, regional demand, category mixes and retailer choices revealed where India’s CPG market is truly heading. This week’s newsletter captures those signals with clarity, but the full report contains the real competitive edge.

Here is your preview.

A Methodology Built for Truth, Not Assumptions

Before we step deeper, you should know how this intelligence was gathered.

Not from surveys.

Not from hunches.

But from millions of real transactions, captured through Bizom’s ever-listening ecosystem: outlet orders, retailer behaviour, distributor velocity, Bizom One marketplace trends, and a blend of public signals like satellite mappings, socio economic clues, and micro market breadcrumbs.

Every number is anonymised, aggregated, and kneaded through bottom up models that treat each category like a breathing organism.

There is no make believe here. Only verified pulse.

A Country Moving in Two Directions at Once

India’s FMCG market rebounded to 6.8% growth, up from just 2.4% in September. Yet beneath this promising headline, a deeper transformation was visible. Urban India grew 6.3%, while non-urban India outpaced it at 7.1%.

Within categories, the hierarchy was unmistakable.

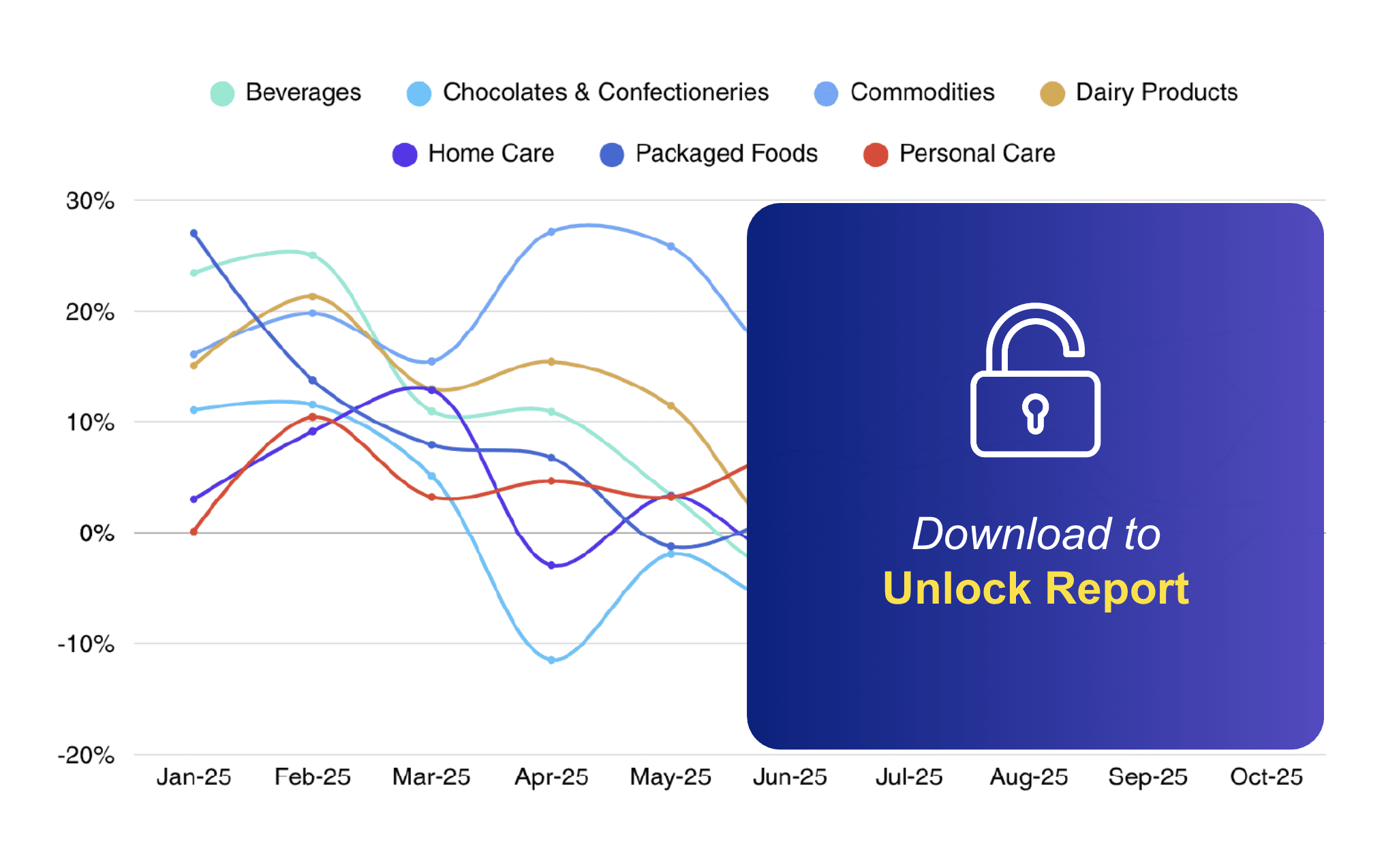

The most striking signal of October came from Dairy. It did not simply grow; it surged at 18.6% YoY, with urban India posting an extraordinary 24.9% increase. Ghee alone commanded nearly half the category’s share.

Personal Care followed with a strong XX% expansion, driven by the combined weight of skincare, oral care and hair care.

Chocolates and Confectionery held their momentum at XX%. The most interesting aspect was the surge in non-metro towns, where growth reached XX%, signalling that modern gifting habits are no longer driven only by urban centres.

Commodities grew XX%, supported by edible oil stability and strong stocking in spices, grains and flours. Packaged Foods grew at a moderate XX%, influenced by a shift toward home cooking in metros.

Home Care stabilised at a minimal X%, lifted mildly by festive cleaning rituals but held back by softer rotation in core categories such as floor and toilet cleaners.

The only category that slipped was Beverages, declining X% YoY, with urban India seeing a sharper minus X% correction. After months of strong summer-led consumption, October signalled a clear cooling in impulse-driven purchases.

To get complete insights, click here!

The Investment Patterns Behind the Shelves

Trade investment patterns revealed the real competitive tactics of October.

In Beverages, brands leaned heavily into small packs with +6.02% YoY growth and mid packs at +9.40% , while large formats declined 2.26%.

In Commodities, Masalas saw large-pack spends jump 1.4%, but Oils declined across small, medium and large sizes, signalling price-stability discipline.

Fabric Care remained a brand-favourite with strong trade support: +XX% in small packs, +XX% in medium, and a minimal +XX% in large.

Dishwasher Liquids did the opposite, with large-pack spends dropping X%, hinting at recalibrated priorities after earlier inventory pushes.

In Packaged Foods, Snacks & Biscuits saw high-rotation packs increase up to X%, while Spreads & Sauces received heavy backing across sizes, rising up to X% in large formats.

Skin Care brands went all-in on penetration, raising small-pack spends X%, while cutting medium and large formats.

These numbers reveal exactly where brands defended their turf, where they probed for expansion, and where they quietly stepped back to protect margins.

To get complete insights, click here!

The Cities and Towns That Led the Month.

While metros like Delhi NCR, Mumbai, Bengaluru and Hyderabad drove performance in categories such as Dairy, Personal Care and Packaged Foods, the real momentum pockets appeared beyond them.

Non-metros such as Lucknow, Jaipur, Mysore, among others, emerged as high-rotation centers across multiple categories. These markets now shape national volume growth as strongly as metros.

The full report breaks down leadership by category, showing which cities are setting the tone for 2026.

The Full Report Holds the Real Power.

The complete Kirana Pulse is not a single-month snapshot. It is a 10-month intelligence vault that captures every shift in India’s CPG landscape from January to October 2025.

One edition. Ten months of verified retail behaviour. A full-market lens that no other platform in India can offer.

Bizom’s vantage point makes this possible. Our ecosystem spans across:

35+ countries

750+ brands

300,000+ distributors

8 million+ retailers

250,000+ sales reps

20 billion USD+ in annual GMV

It is why the Pulse sees inflection points long before they appear in sales reports. When you study the full edition, you are not just reading market data, you are reading the real behaviour of India’s CPG engine, captured at national scale.

The full report brings together October’s shifts with month-by-month patterns across 2025, delivering:

- Clear category-wise growth movements across Dairy, Personal Care, Commodities, Confectionery, Packaged Foods, Home Care, and Beverages

- Deep subcategory splits that highlight which segments carried the month’s momentum.

- Top-performing cities and non-metro clusters used by brands for planning

- Regional shifts across India’s North, South, East and West markets, split by urban and non-urban demand

- A view of category resets compared with previous months

- Movements in trade spends across pack sizes

- Changes in kirana reach that reflect real channel penetration

If your decisions depend on understanding where demand is flowing, which formats are winning and which micro-markets are quietly reshaping national trends, you will want the full Pulse.

Your first look at India’s hottest CPG shifts starts here.